ServiceChannel

Modified on

April 22, 2025

Table of Contents

The pandemic has trained more of us to meet our basic banking needs online or through a mobile app. Boston Consulting Group found that one in four people planned to visit their branches less or not at all when the crisis is over, with the virus making them wary of public spaces.

At the same time, research has shown that consumers prefer to use a branch when opening new accounts, and that branches play an outsized role in customer satisfaction. With time spent in banks now under threat, banks must prioritize a flawless experience to maintain a steady flow of in-person business – and assuming greater control of facilities management is a critical step.

Most banks outsource the repair and maintenance of branches to an integrated facilities management company, or IFM. It’s an alluringly simple model, but handing over this work to a third party leads to higher costs, greater risk, and less control over the customer experience. It also holds back wider efforts at digital transformation, because banks lose access to the data needed to optimize operations.

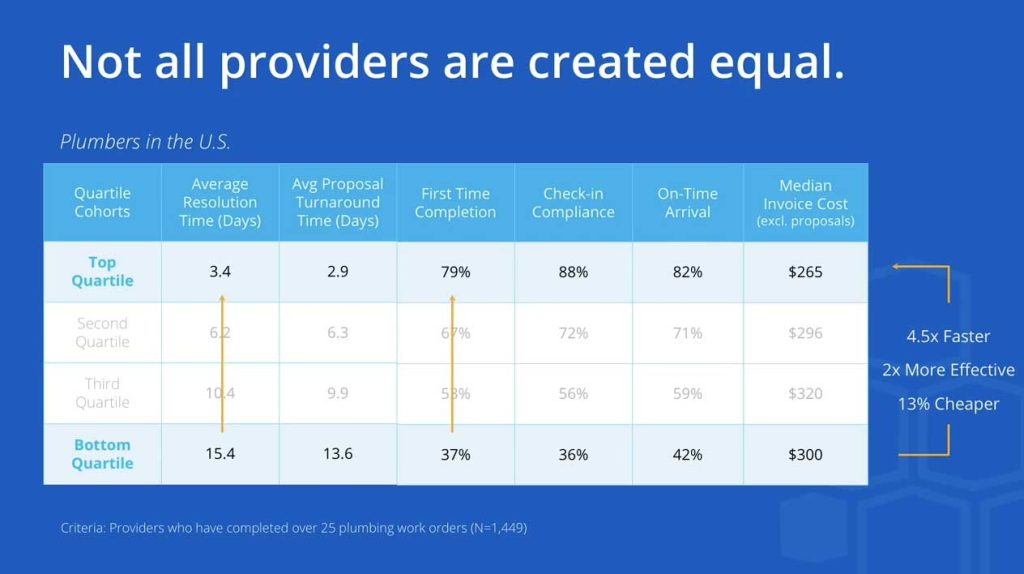

Here are 4 reasons why banks should take back control of their facilities management to boost efficiency and customer satisfaction:

Transparency. Outsourcing is the ultimate black box. Banks have no visibility into how much of their spend actually goes to contractors who do the work versus being funneled off in management fees. At ServiceChannel, we occasionally do assessments to determine how much of the spend goes directly to repair and maintenance. In some cases, that figure is as low as 51%, meaning half of what banks are spending is eaten up by fees, markups and other costs. In addition, banks have no visibility into whether they are getting the best value or quality of work available in any given city or state.

Security. Banks should know who walks in and out of their branches and how much time they spend there. Branches know which customers and employees walk through the door, but they have no idea exactly who fixes the A/C, repairs the plumbing or cleans the bathrooms. Have these providers been vetted? Did the IFM conduct background checks?

Taking ownership allows a bank to hand-pick trusted service providers who vouch for the credentials of their staff. Authentication technologies in modern facilities management systems also verify that the person who walks through the door is who they say they are, and produce an audit trail of exactly who was on site and for how long. With an IFM, banks get nothing but assurances that the workers assigned to them are trustworthy, which is an unstable foundation for good security and governance.

Risk management. Being beholden to a single provider is never a good thing, yet many banks are entrusting the upkeep of their entire branch network to a single IFM. That company could go out of business, get acquired or raise prices at any time. It also has no meaningful competition, which means work quality can suffer.

Banks should have a network of contractors they can turn to as needs dictate. If demand spikes unexpectedly due to a severe weather event or an outbreak like COVID- 19, the bank can hire from an extensive network instead of being tied to an IFM that may say, “Sorry, we have no capacity this week.” If a branch can’t stay open, that’s a week it won’t be serving customers and capturing deposits..

Digital transformation. The larger goal for every modern business is to have data and digital technologies drive every aspect of cost, performance and customer satisfaction. Banks have been on the cutting edge of this trend, yet management of their physical branches has been largely left out.

The key to optimizing branch operations is data, which allows for smarter decisions about repairs, maintenance and equipment. Tracking granular data on provider responsiveness, speed and costs allows you to hold them to account for their work. Repair history tells you when to replace a piece of equipment instead of having it fixed for the umpteenth time. And data can predict when equipment is likely to fail, so it can be replaced in time to avoid unnecessary closures.

Outsourcing to an IFM cuts off access to all this data. In fact, you’re handing your data over to a third party which can use it to improve their own business — and paying them for the privilege. Data is fundamental to digital transformation, and physical branches should be a part of that modernization.

Summary. It’s time for banks to take back control of their physical assets. The spend without control, without data, and without oversight must end. Branches are the public face of a brand, and the impression they make on consumers will have a significant bearing on business in the months and years ahead. They should be serviced by providers who have to compete to keep your business every day.